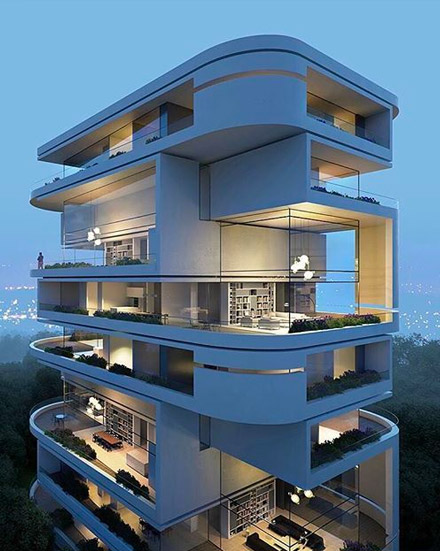

Mortgage Programs & Financing Options for Kennedale Oaks Townhomes (DFW)

Buying a $500,000+ new-construction townhome at Kennedale Oaks (planned for late 2026 move-in) starts with one decision: choosing the right financing path for your situation—first-time buyer, move-up buyer, or investor. This guide covers the main mortgage options, Texas down payment assistance programs, and how to prepare early so you can close with confidence.

Key Takeaways

- Multiple mortgage programs are available for Kennedale Oaks buyers, including conventional, HomeReady, Home Possible, and Texas down payment assistance options.

- Planning early for a 2026 move-in allows buyers time to improve credit, strengthen purchasing power, and secure the best financing terms.

- Pre-qualification now helps buyers lock in eligibility, compare loan programs, and move confidently when construction completion approaches.

Start Here: Conforming Conventional Loans (Most Buyers)

Most Kennedale Oaks buyers will use a conventional conforming loan. These loans follow FHFA limits and can be acquired by Fannie Mae or Freddie Mac, which often supports competitive pricing. For 2026, the FHFA baseline conforming loan limit for a one-unit home is $832,750 in most U.S. counties. Verify 2026 conforming limits.

For a $500,000 purchase, conforming financing typically applies unless you are borrowing significantly above the conforming limit (which would be uncommon at this price point).

First-Time Buyers: 3% Down Options (HomeReady & Home Possible)

- If you qualify by income, you may be able to buy with as little as 3% down using:

Fannie Mae HomeReady (income at or below 80% AMI, minimum credit score commonly 620, principal residence). HomeReady overview. - Freddie Mac Home Possible (income at or below 80% AMI, principal residence; lender credit-score requirements vary). Home Possible overview.

These can be strong alternatives to FHA for many buyers because they can offer low down payments and the ability to remove mortgage insurance later, depending on your loan structure and equity.

Texas Down Payment Assistance (DPA) What You Should Know

- Down payment and closing costs are the biggest barrier for many buyers. Here are reputable Texas resources to explore early:

TDHCA – My First Texas Home: offers flexible down payment and closing cost assistance (often shown as 2%–5% of the loan amount) and includes options like a 3-year deferred forgivable second lien in certain structures. TDHCA program details. - TSAHC: offers mortgage loans paired with down payment help (grant or second lien options depending on program and eligibility). TSAHC down payment assistance.

- Tarrant County Homebuyer Assistance (Housing Channel): may provide up to $50,000 in down payment and closing cost assistance for eligible first-time buyers purchasing in Tarrant County. Tarrant County assistance overview.

Most DPA programs require income eligibility, a minimum credit score, a primary-residence purchase, and completion of a homebuyer education course. The best next step is to speak with a lender who regularly closes TDHCA/TSAHC/DPA transactions.

Move-Up Buyers: Two Smart Paths

- Use equity from your current home for a stronger down payment (often reduces monthly costs and may remove mortgage insurance sooner).

- Plan your timeline early: because Kennedale Oaks targets late 2026 move-ins, you have time to improve credit, reduce debt, and increase cash reserves.

Investors: Expect Higher Down Payments

Investment-property financing is typically stricter than owner-occupied. While exact requirements vary by lender and market conditions, many investor loans require a larger down payment and stronger reserves. If you are purchasing as an investor, ask your lender about: required down payment, reserve requirements, and whether the property type is treated as townhome/condo for underwriting purposes.

2026 Planning Checklist (Do This Now)

- Credit: aim to keep utilization low, avoid late payments, and reduce revolving balances.

- DTI: reduce monthly debt payments before applying to expand buying power.

- Cash strategy: budget for down payment + closing costs + reserves.

- Program eligibility: confirm AMI limits for HomeReady/Home Possible and income limits for DPA programs.

- Lender match: choose a lender experienced in new construction timelines and Texas DPA programs.

Next Step: Get Pre-Qualified and Track Availability

The smartest buyers start the financing conversation early—especially with a late 2026 move-in target. If you want help reviewing your best loan path, down payment assistance options, and next steps for Kennedale Oaks, connect with the listing team today.

CALL MARCELLA RICHARDSON

(682) 772-5784

MarcellaRichardson@kw.com

Prefer to schedule online? Visit:

https://kennedaleoaks.com/contact/

Frequently Asked Questions

What mortgage is best for a $500,000+ Kennedale Oaks townhome?

Many buyers use a conventional conforming loan. First-time buyers may also qualify for 3% down options like HomeReady or Home Possible if income limits apply.

Are there down payment programs in Texas for DFW buyers?

Yes. Start with TDHCA and TSAHC, and review Tarrant County assistance through Housing Channel if you qualify.

When should I start the mortgage process for a 2026 move-in?

Start now with pre-qualification and program eligibility. Most buyers complete final underwriting closer to completion, but early planning improves approval odds and options.

“Financing preparation is one of the most important steps when buying new construction. With Kennedale Oaks offering a limited collection of just 39 modern townhomes, buyers who start the mortgage and pre-qualification process early position themselves for the best options and timelines. Call me at (682) 772-5784 and I’ll help guide you through availability and next steps.”

Marcella Richardson | Licensed Realtor

Keller Williams Lonestar DFW